When Actual Sales Are Greater Than Production

The firm should take as few risks as possible. When actual sales are greater than forecasted sales.

The High Low Method Accounting Basics Method High Low

Sales volume activity variance.

. Ending inventory is greater than the beginning inventory the operating income under absorption costing is greater. A Inventory will decline B Production schedules might have to be revised upward C Accounts receivable will rise D All of the options are true. There are four types of profit variance which are derived from different parts of the income statement.

If the Actual cost is higher than the standard it creates an. What actual sales are greater than production. 200 x 40 8000 F 88000 80000 Sales price variance.

A profit variance is considered to be favorable if the actual profit is greater than the budgeted amount. Favorable budget variances occur when the actual results are better than the amount budgeted. Production schedules might have to be revised upward.

Sales greater than Production. The cost is fixed and the actual production was less than budgeted production E. Production schedules might have to be revised upward.

See the answer See the answer done loading. When actual sales are greater than forecasted sales A. Unfavorable variance is an accounting term that describes instances where actual costs are greater than the standard or projected costs.

For example if i create order of 1000 EA and create delivery w r t this order system brings this 1000 EA quantity and if i change the order quantity. All of the above. When actual sales are greater than forecasted sales a.

Budget materials purchases equal to the current months needs for production. Standard costs are the estimated costs of labour material and other costs of production. Actual Costs on the other hand are those realized during the period and compared at the end of the period.

Accounts receivable will decrease. Profit variance is the difference between the actual profit experienced and the budgeted profit level. All of the other answers are correct.

Accounts receivable will rise. 200 more fewer items were sold. The total variance between original budget and actual sales is 5000 F This has been caused by.

The cost is variable and actual production was 90 of budgeted production D. Manufacturing costs are less than the amount budgeted. Greater than net income under absorption costing method.

Accounts receivable will rise. When actual sales are greater than forecasted sales. Reported revenues are more than planned revenues.

Financial managers can analyze the data to consider if a favorable. The same as net income under absorption costing method. Production schedules might have to be revised upward.

Budget unit production for the month at greater than budgeted unit sales for the month. If actual volume is lower than actual volume at budgeted mix the formula will give a negative result and the sales mix variance is said to be unfavorable. If actual volume is greater than the actual volume at budgeted mix the sales mix formula gives a positive result and the sales mix variance is a favorable variance.

Examples of favorable budget variances include. When actual sales are greater than forecasted sales a. Production schedules might have to be revised upward.

What effect do seasonal sales have on inventory in a company that uses level production schedules. Production volume variance is a statistic that measures the overhead amount that is applied to the actual number of units of a product produced. When actual sales are greater than forecasted sales what happens to the level of inventory accounts receivables and.

Prepare production budgets without a sales forecast. When production is equal to sales meaning there is no difference in the beginning and ending inventories the operating income under both methods are the same. The cost is variable and actual production equaled budgeted production C.

If sales equal production one would expect net income under the variable costing method to be A. See the answer. Inventory will decrease and accounts receivable will increase.

When a company sells more than it produces during the current period this indicates it is selling goods produced in a prior period. Production schedules might have to be revised downward. Quorum Company desires an ending inventory of 120000.

Accounts receivable will rise. This will result in net income under variable costing being greater than under absorption costing. Under absorption costing opening inventory carries with them a part of fixed manufacturing overhead of the previous period.

Expenses are less than the planned budget. While creating delivery with reference to order if one changes the delivery quantity manually then system allows changes this results in sales order quantity to be lesser than delivered quantity. If sales are more than the production variable costing will show higher net income than the absorption costing.

When production is greater than sales ie. An unfavorable variance can alert management that the. Production volume variance helps corporate managers.

Less than net income under the absorption costingmethod. The cost is variable and actual production was 80 of budgeted production B 19. They are noted below.

Proper risk-return management means that a. Instead of earning 88000 on sales of 2200 only 85000 was generated. Differing in as much as the difference between sales and production.

Selling more than was produced means that units in the opening stock are being sold. This difference between the standard cost vs actual cost is termed as Variance. This problem has been solved.

When production units is greater than sales units absorption costing net income will be. A- greater than variable costing net income B- equal to variable costing net income C- lower than variable costing net income D- there are not relation between two methods. Accounts receivable will rise.

As sales decline inventory will increase. 8132018 Assignment Print View 7. Accounting Cost Accounting Financial Accounting CMA Costing.

Break even sales - Fixed cost contribution margin ratio Break even sales 600000 03 2000000 Margin of safety actual sales - breakeven sales Break even sales margin of safety Actual sales 2000000 02actual sales Actual sales if actual sales 1 then 2000000 02 1 2000000 08 actual sales actual sales 2000000 08 actual sales.

Pin On Thought Leaders

If You Can Make Better Business Intelligence Resume You Will Be Better Than Other Candidates And You Ll Be Chosen For The Position You Need Actual Check M

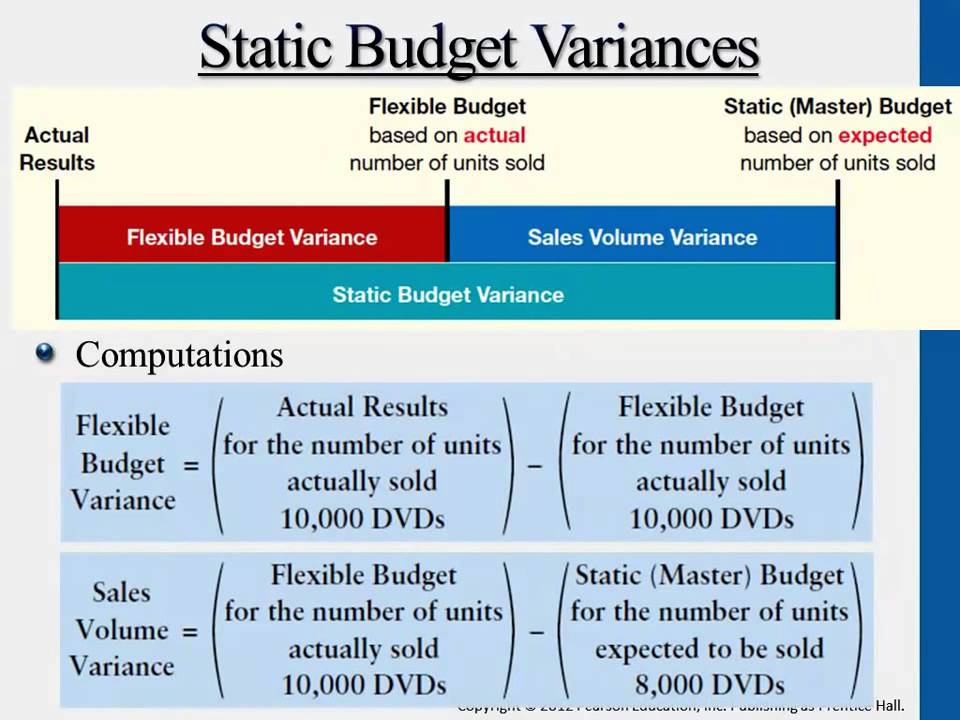

Static Budget Variances Managerial Accounting Kavan Ingram I Like This Video For Static Budget Variance Because Budgeting Managerial Accounting Flexibility

No comments for "When Actual Sales Are Greater Than Production"

Post a Comment